“For overseas groups, UK audit obligations are shaped by the group as a whole, not just the size of the UK subsidiary.

UK statutory audit requirements for overseas groups: what finance teams need to know

28 April 2026

For overseas groups with UK subsidiaries, audit and reporting obligations are rarely top of the risk agenda. UK entities are often small relative to the wider group, well‑run, and historically able to rely on exemptions or streamlined reporting.

However, that landscape changed materially following the UK’s departure from the EU.

Post‑Brexit legal changes, combined with updated international auditing standards, mean many overseas groups are now unexpectedly within scope of a UK statutory audit – frequently discovering this late in the reporting cycle, when options are limited.

This article outlines how UK audit requirements apply to subsidiaries of overseas groups, why historic exemptions are no longer available for many EU‑owned entities, and what finance leaders should be considering now to avoid disruption.

UK statutory audit requirements: why group size matters more than local turnover

Under UK law, most companies must prepare audited financial statements unless they qualify for a specific exemption. Certain small companies may be exempt, as explained in our earlier article on UK audit thresholds.

For overseas groups, however, the calculation is rarely as simple as reviewing the UK entity in isolation. In practice, many UK subsidiaries fail to qualify for exemption because:

Group‑level size tests apply, not just the subsidiary’s own results

Overseas parent companies are included when assessing thresholds

Shareholder rights, group structures or regulated activities can trigger audit requirements regardless of size

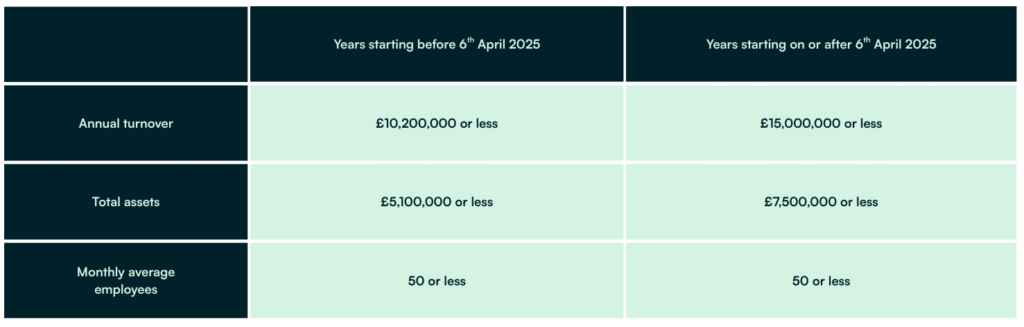

Below is a summary of the group wide size limits

The consequence is that UK statutory audit requirements frequently apply even where the UK operations are modest. This often comes as a surprise to overseas finance teams who are accustomed to different jurisdictional rules.

Group reporting and audit coordination under the revised ISA 600

Where an overseas parent prepares consolidated financial statements, the UK subsidiary will typically be required to support the group audit process, including:

- Preparing group reporting or consolidation packs

- Supporting component audit procedures

- Working to group reporting timetables that may not align neatly with UK statutory deadlines

Recent changes to ISA 600 (Group Audits) have increased the focus on consistency, documentation and cross‑border oversight. While UK statutory audits and overseas group audits remain legally separate, effective coordination between the two has become essential.

From a practical perspective, early engagement between the UK statutory auditor and the group auditor can:

- Reduce duplication of audit work

- Avoid conflicting information requests

- Ensure both UK filing deadlines and group consolidation timelines are met

In our experience, issues rarely arise from the audit itself, but from late planning and poor alignment across jurisdictions.

The loss of the UK audit exemption for EU‑owned subsidiaries

Prior to Brexit, many UK subsidiaries of EU groups relied on the Companies Act s.479A parental guarantee exemption, where an EEA parent prepared consolidated accounts deemed “equivalent” under UK law.

However, following the UK’s departure from the EU:

- EU‑established parents are no longer treated as preparing “equivalent” consolidated accounts

- As a result, UK subsidiaries of EU groups can no longer rely on the s.479A exemption

Several years on, this remains a live issue. Many EU‑owned UK entities are still operating on legacy assumptions, only discovering the impact when statutory deadlines approach. In most cases, the only solution is the appointment of a UK statutory auditor.

What good looks like for overseas groups with UK subsidiaries

Well‑managed overseas groups tend to share a few common characteristics:

- They review UK audit requirements when group structures change, not just at year‑end

- They plan UK statutory audits alongside group audit processes

- They work with auditors who understand both UK compliance obligations and international group reporting pressures

Taking a proactive approach allows UK compliance to be predictable, proportionate and efficient, rather than reactive and disruptive.

How Affinia supports international groups

Affinia works closely with UK subsidiaries of overseas groups, from first‑time statutory audits through to complex group reporting environments.

We offer:

- Statutory audits proportionate to the size and risk profile of the UK subsidiary

- Pragmatic, high‑quality audit work focused on clarity and risk management

- Seamless collaboration with overseas group auditors, including Big Four and mid‑tier firms

- Delivery aligned with Companies House deadlines and group reporting cycles

- Clear, proactive communication that supports finance teams operating across jurisdictions

- Insightful feedback on systems, controls and governance within the UK entity

Our aim is not simply to complete a UK audit, but to make UK compliance straightforward, efficient and beneficial for overseas parent groups.

Oliver White

Director, Audit & Assurance

Meet our Audit experts

Previous slide

Next slide

More Thought Leadership

Uncategorized

The rise of payroll risk reviews: What independent assurance reveals

June 30, 2026

Thought Leadership

Strengthening trust: what the SRA’s Accounts Rules reforms mean for law firms

June 18, 2026

Thought Leadership

Automation isn’t enough: Why Payroll success requires more than great software

June 16, 2026